Is China Up Next and Should You Hedge? (July 31-August 4)

July 31-August 4, 2023 by Adit Dayal for RIPPYGLOBAL.

Happy Sunday everyone and welcome back to the Rippy Global weekly outlook. Last week which was full of catalysts ended up with the S&P 500 closing around +1%. What is expected to be the last rate hike in this cycle of Fed tightening was (predictably) announced on Wednesday bringing the Fed Funds Rate to the highest it’s been in 22 years. In surprise to the markets, the Bank of Japan moved their monetary policy to one that is tighter and more in line with other countries causing a bit of shock to the markets.

Demand for the dollar is beginning to drop as investors believe that the Fed is done hiking rates which is a top indicator that risk is on in the stock market.

Let’s take a look at this week!

——-

Along with the catalysts listed above, we also had some other economic data that drove the markets higher. Notably, US GDP grew at 2.4% which is +0.9% higher than expected according to the Bureau of Economic Analysis. The CPE inflation number also showed cooling with a number of 3.0% vs. 3.8% last month. This is the Fed’s preferred method of gauging inflation. Powell spoke and cited that he hopes this trend continues which then led the expected probability of a hike in September to drop to 18% from 22%.

Earnings were big in the headlines and it will continue to be that throughout this week with the largest company in the S&P 500 reporting this week (Apple).

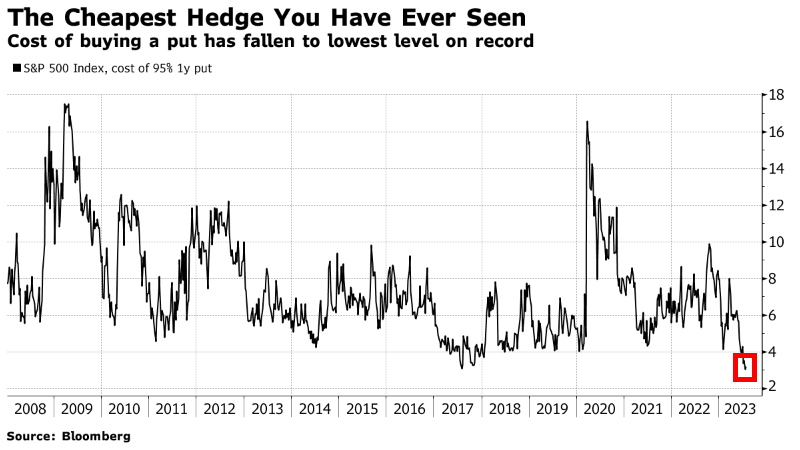

According to the Bank of America equity team, it has never been cheaper to hedge against the stock market with the cost of a 1Y put option on the S&P 500 at the cheapest it has ever been in recent history. The cite the yield curve still being inverted by 90pts being hedged with an interesting trade of a year dated put spread that can return with an 8 to 1 max risk/reward.

Earnings were heavily driven by AI expectation and eyes are going to be on semiconductor names but I think it’s time we have a warning here with Intel and Samsung both saying that the semiconductor shortage is waning with the AI demand not being a large part of the shortage anymore. The Intel CEO did say that an inventory shortage in CPU’s is expected to continue into the 3rd quarter and he expects chip sales to slow as well.

Chinese stocks have been flying recently, kicked off with ANT groups expectation of stock buybacks and then bolstered with investment in LI Auto. With expectations that the Chinese authorities will deliver on bolstering growth for companies there, I am expecting continuation from those names this week.

This next sector isn’t one I usually talk about, but I did think this report from activist fund Starboard Value was interesting with them seeing huge potential in the restaurant industry which he think has overreacted. Their recent investment on $CRM has gained 54% since they announced a stake. I will watch these food stocks this week to see if this headline drives any volume.

With energy being the worst performing sector so far in 2023, halfway through the year may be a good time to look at the bull case here.

nsider buying in energy names was the highest in July when compared to other sectors. Legendary investors like Warren Buffet are buying heavily into names like Occidental Petroleum, and according to MarketWatch, most energy names are actually discounted from their trailing 5yr P/E ratio by anywhere from 30-80%. Goldman Sachs analysts expect an upcoming energy deficit driving the price of oil to $86/bbl by the end of the year.

——-

#1) Earnings week continues into next week with Wednesday being huge for financial names like PayPal and Robinhood and Thursday with Apple and Amazon reporting after the bell.

#2) On Tuesday, Chinese EV stocks will report delivery numbers and it will tell us if there’s an end put on this rally here or if they will continue their gain.

#3) On Wednesday, DDOG will have their annual investors event and Costco is expected to report their monthly sales after market close.

#4) On Thursday, the market will be waiting on Apple and Amazon’s reports after close for garages on technology and consumer sentiment but FSR which has high short interest is showing off their product portfolio after market close.

#5) On Friday, the US jobs report is releasing for July at 8:30 AM with an expectation of 200K jobs added.

——-

S&P 500

The S&P 500 ($SPX index) is chopping around with mixed data. I am expecting abbot of a short squeeze from short who got trapped on Thursday and then a cool off with further direction being determined by the earnings reports later in the week.

My key breaks are $4590 for bulls and $4567 for bears.

The best ways to play the S&P 500 are via. SPY/SPX options or SPXL (3X Bull S&P 500 ETF.

——

INDIVIDUAL STOCKS & LEVELS

Let’s recap some of the levels of some popular names:

TSLA

This name is still chopping after a huge run which is healthy. As I mentioned last week, I want to see it hold the $247 low for continuation to fill the gap to the upside.

AAPL

I don’t even feel like this stock is worth trading at all this week with unexpected price action and overpriced options due to earnings this Thurday making this huge run either validated or can lead to a huge sell off that will drag the market down with it.

KC

With China names moving strong, I really like this one which has been showing huge accumulation and call option buyers in the $15 strike which is over 100% out of the money.

——-

Insider Activity

In terms of insider trades, ABOS got a huge buy this week, but I really like ASAN as an under the radar insider swing trade. This name has been getting huge hits recently and may be due for a rally.

——-

High Short Interest Stocks (S3 Data)

#1 - ALLO 53% SI

#2 - CVNA 47% SI

#3 - LCID 41% SI

#4- SYM 40% SI

#5- UPST 39% SI

——-

Thanks for reading this weekend’s article, have a great week!

-Adit Dayal (https://twitter.com/tradelikehulk)